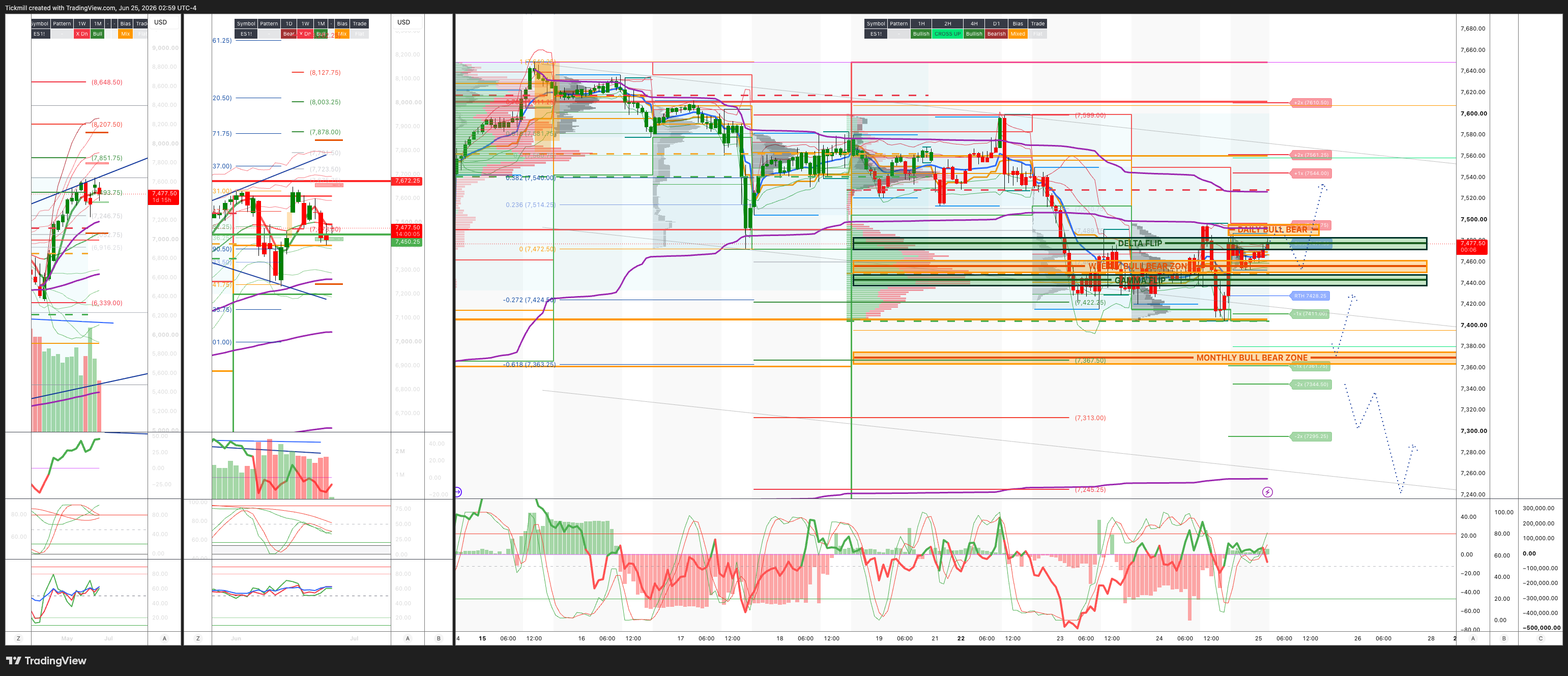

S&P500 Daily Action Areas & Price Targets 25/6/26

S&P500 Daily Action Areas & Price Targets 25/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7560/50

WEEKLY RANGE RES 7692 SUP 7448

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.20 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7496

WEEKLY VWAP BULLISH 7494

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - BALANCE - 7496/7404

WEEKLY STRUCTURE - BALANCE 7648/7247

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7490/7500

GAMMA FLIP 7451

DELTA FLIP 7478

DAILY RANGE RES 7545 SUP 7409

2 SIGMA RES 7613 SUP 7341

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

SHORT ON REJECT/RECLAIM DAILY/MONTHLY BULL BEAR ZONE TARGET RTH CLOSE

LONG ON ACCEPTANCE ABOVE DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

JPMorgan TRADING DESK VIEW

The market remains tactically constructive, but the message from the last several sessions is that leadership is narrowing again and the AI complex is becoming more volatile as positioning gets more crowded. The post-Iran MOU “everything rally” is fading into a more selective tape, with investors returning to the Tech/cyclical barbell and putting more emphasis on direct AI infrastructure, memory, custom silicon, power, utilities, financials, defense, and quality growth. Lower oil remains the key macro offset to Warsh’s more hawkish Fed, helping reduce inflation risk and supporting consumers, but policy uncertainty has replaced geopolitics as the primary macro risk.

The MU/memory commentary was fundamentally very supportive. The additional disclosure around supply agreements is important because the largest agreements appear to include ceiling prices tied to current CQ2 market prices and floor prices through the term of the agreement. That gives investors more confidence around revenue visibility and pricing durability. Management’s message was also clear that the industry remains in the early innings of AI-led innovation and productivity, and that even with gradual supply improvement in 2028, there is still no clear line of sight on when memory supply can catch up with demand. The structural supply story remains favorable because meaningful growth increasingly requires greenfield fabs, technology transitions are slowing bit growth over time, and NAND capacity is being redirected toward DRAM.

That supports the bull case for memory, but the tactical setup is more complicated because memory is now the most consensus long within AI. DRAM has seen roughly $3bn of inflows over the last week and $8.5bn over the last month, putting it near the top of fund leaderboards alongside the largest index products. That is powerful sponsorship, but also creates sell-the-news risk after the recent Korea and SOX volatility shock. The fundamental story remains intact, but the market’s tolerance for disappointment has clearly fallen as positioning has become more extended.

Dubravko’s mid-year outlook reinforces the earnings-led bullish equity case. The YE26 SPX target rises to 7,800 from 7,600, implying roughly 5.9% upside from the June 23 close. The key driver is the scale of SPX earnings upgrades, with FY26 and FY27 consensus EPS up around 10%, which is historically unusual outside of post-shock or post-recession periods. The forecast now looks for 2026 SPX EPS of $350, up 29% year over year, and 2027 EPS of $390, up another 15%. The longer-term message is that fundamentals resemble an early-cycle growth profile rather than a late-cycle exhaustion profile.

The preferred equity implementation remains quality-oriented. The bias is toward Quality Growth, direct AI plays, and Low Vol, while the biggest reversal risk sits in Low Quality and Speculative Growth. Sector preferences remain Tech, upstream AI beneficiaries such as Utilities and select Industrials, Banks, Defense, and growth areas of Healthcare including Biotech, Equipment, and Life Sciences. Energy is flagged as ripe for profit-taking despite still being the cleanest geopolitical hedge, which makes sense given the sharp reversal in crude and the downgrade to the oil outlook.

Bram’s derivatives outlook is consistent with a constructive but volatility-aware market. He expects volatility to decline from the first half to the second half, while vol-of-vol remains elevated. That supports carry and upside structures, but argues against complacency because volatility shocks can still be abrupt. The preferred Tech expressions are NDX over SPX or XLK over SPX outperformance calls, reflecting continued AI and Tech leadership. Selling GOOGL and MSFT puts as target-buy structures also fits the current setup, using the technical pullback and richer volatility to build exposure in higher-quality platform names at better effective entry levels.

Financials remain a favored upside expression into Q2 bank earnings, with XLF calls preferred as fundamentals in capital markets and trading remain constructive. This also fits the positioning backdrop, where Financials remain under-owned despite recent interest. Low Vol and Utilities are another important leg of the equity view, with JPAMLVAR calls or JPAMLVAR over SPX outperformance calls and XLU call spreads attractive given AI-related power exposure, inexpensive vol, and relatively flat skew. The hybrid idea of buying SPX or NDX calls contingent on rates up is also notable, as it expresses a positive equity outlook in a hawkish rates environment where realized equity-rates correlation has been strongly negative.

Natasha’s oil outlook has turned materially more bearish and is important for both macro and sector allocation. Brent is now forecast to average $86 in 3Q26, $80 in 4Q26, exit 2026 at $78, and average $64 in 2027. The driver is weaker-than-expected OECD inventory draws and demand losses, particularly in China. The key point is that Chinese oil demand appears to have fallen much faster than expected, suggesting the economy may be adapting to higher energy prices more efficiently than prior experience would imply. If durable, crude import requirements could be as much as 1mbd below prior assumptions, requiring much smaller inventory drawdowns going forward.

For equities, lower oil is a meaningful support because it offsets part of the hawkish Fed impulse and improves the inflation and consumer backdrop. For Energy equities, however, it creates profit-taking risk. Energy still has value as a geopolitical hedge, but if the market is aggressively fading the war premium and the 2027 Brent forecast is moving toward the mid-$60s, the sector’s relative earnings momentum becomes harder to defend. The oil move is therefore bullish for the broader market but more challenging for Energy leadership.

The ETF desk commentary shows that investors are becoming more selective in buying dips. The sharp move lower in EM and Korea should have attracted stronger demand from investors with conviction, but interest to reload longs was only sporadic. That is a notable divergence from prior pullbacks, which were quickly bought. It suggests the Korea/Semi shock has affected investor psychology, even if the broader AI theme remains intact. At the same time, DRAM remains extremely popular with clients, underscoring the split between caution on levered Asia/EM exposure and continued conviction in the memory shortage theme.

Gold and miners remain under pressure, with spot gold breaking below 4,000 and the desk seeing hedge fund selling in GDX. That fits the broader post-MOU, stronger-dollar, lower-geopolitical-risk backdrop. As oil’s war premium fades and the dollar remains supported by Warsh’s Fed, the urgency to own gold as a hedge has diminished. The weakness in gold is less about a broad macro crisis and more about risk premium compression and USD strength.

The AVGO update is one of the more important positives for the AI infrastructure thesis. The company announced a long-awaited new win with a frontier model leader, with first samples of the Jalapeno chip now received and under test. Hock Tan indicated the accelerator is showing roughly 50% cost savings versus typical AI GPUs, and shipments could exceed the previously soft-guided 1.3GW. The confirmation matters because some Asia sources had suggested the project might have been cancelled, so validating that it is on track removes an overhang.

The AVGO story also reinforces that the AI capex cycle is broadening beyond GPUs. This project appears more networking-heavy and the ASIC is more expensive, implying AVGO content could land near the upper end of its per-GW range. There may also be an ARM ASIC project under test and evaluation with potential purchase orders next year. The broader read-through is that custom silicon, networking, interconnect, power efficiency, and data-center architecture are becoming increasingly important parts of the AI stack. AVGO remains one of the cleaner ways to express that theme.

Consumer price action looks constructive on the screen, but the flow backdrop is less convincing. Lower rates and lower crude are supporting rate-sensitive and high-beta consumer names, with strength in names like W and RH and continued recovery in cruises after the CCL guide-related selloff. WEN’s meme-like move also contributed to the short-squeeze feel. However, desk flows were actually meaningfully better for sale in both Discretionary and Staples, with investors using strength to trim. The few buy tickets leaned defensive, including WMT, USFD, KDP, and HD, while supply was seen in names such as BROS, LEVI, PRMB, CCL, GIS, DKS, and NKE.

That suggests the consumer rally is more mechanical than conviction-led. The bid appears driven by machines, lower yields, lower oil, de-escalation squeeze dynamics, and short-covering, rather than fundamental long-only sponsorship. This does not mean the trade cannot continue tactically, especially if oil and yields keep drifting lower, but it does argue for being nimble in Airlines, Housing, Retail, and high-beta consumer. These trades can work in the post-MOU environment, but historically the rallies are short-lived and vulnerable to headline volatility.

The US Market Intel view remains tactically bullish, unchanged from the June 15 upgrade following the US-Iran MOU. The basic framework is that the MOU reduces downside escalation risk, supports increased oil flows from the Persian Gulf, and keeps the disinflationary impulse intact. However, the desk expects the broad “everything rally” to fade into more concentrated leadership, with MU earnings as the key near-term AI catalyst. The main risk is that semiconductor volatility remains elevated because of crowded memory positioning and the rising use of leveraged ETFs, particularly in Asia.

The monetization framework remains a Tech and Cyclical barbell, but with a preference for US AI over Asia AI after the Korea volatility shock. The desk continues to favor staying long the global AI theme, particularly direct AI infrastructure, semis selectively, custom silicon, networking, utilities and power beneficiaries, and quality growth. Financials remain attractive into July earnings, with strong fundamental growth intact and room for catch-up versus broader cyclicals. Defense and select growth Healthcare also screen well.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!